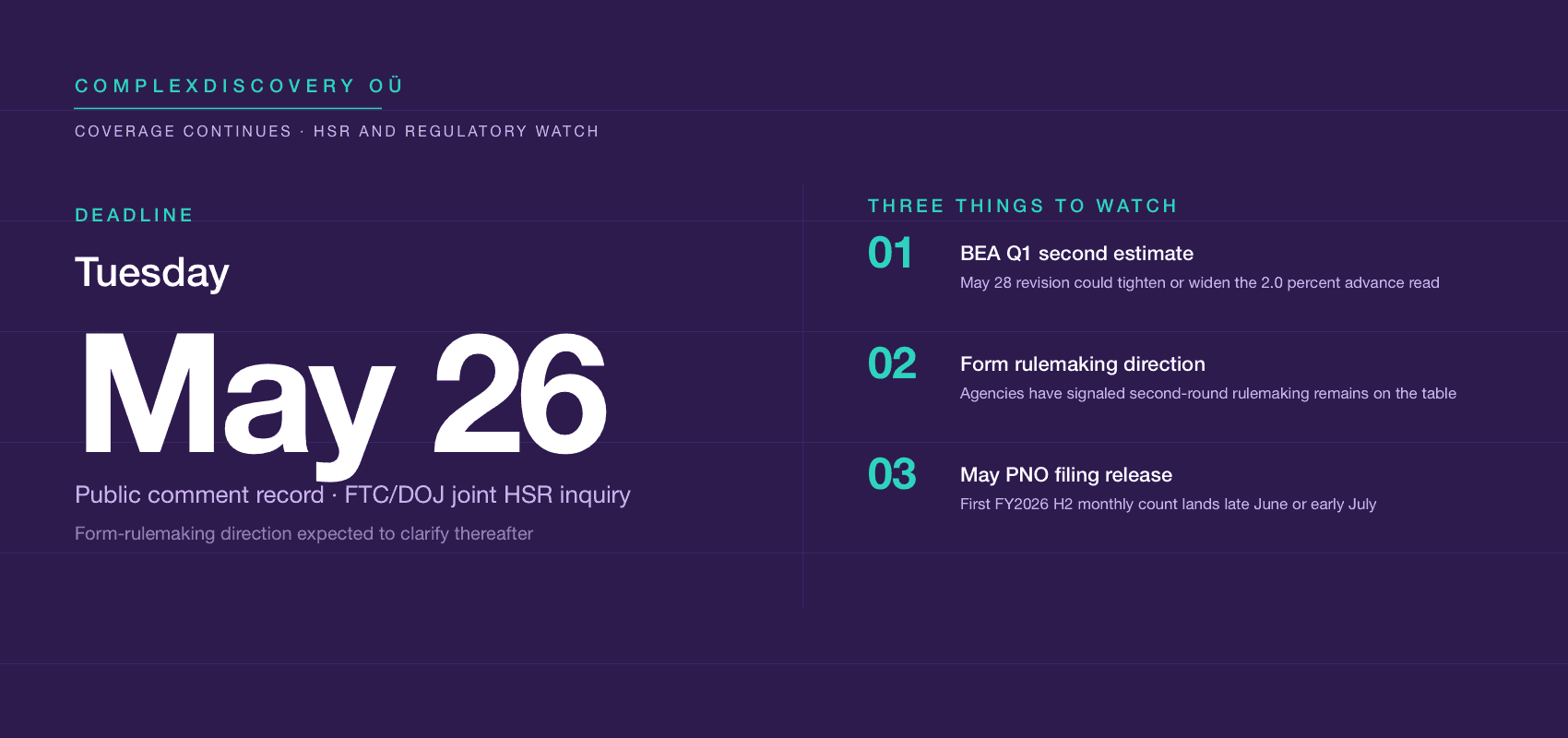

Editor’s Note: The Premerger Notification Office logged 185 transactions in April 2026 — a 9 percent step-down from March’s high of 203 but 58 percent above the 117 filings recorded in April 2025 — lifting the FY2026 running total to 1,430 reportable transactions across the first seven months of the fiscal year. Every month of FY2026 so far has come in at 180 transactions or above, and, if current run-rates hold, the annualized pace would top 2,400 transactions, well above the FY2024 Annual Report total of 1,973 adjusted transactions and on track to outpace the FY2025 preliminary count of approximately 2,101. This edition reads April’s figure in context with three developments shaping the second half of the fiscal year: the Supreme Court’s February 20 IEEPA tariff ruling and its Section 122 replacement regime, now feeding into CBP’s April 20 launch of its consolidated refund processing functionality; the Fifth Circuit’s March 19 decision restoring the pre-February 2025 HSR form, with the joint FTC/DOJ public inquiry closing May 26; and the BEA’s April 30 advance estimate showing first-quarter real GDP at 2.0 percent alongside a 4.5 percent annualized PCE inflation reading.

For cybersecurity, information governance, and eDiscovery professionals tracking Second Request pipeline timing, April’s data points to sustained capacity demand through year-end. Watch the BEA second estimate on May 28 and the form rulemaking that follows the public-comment window.

Industry News – Antitrust Beat

Second request pipeline watch: April HSR filings, Q1 GDP, and form rulemaking window closing

ComplexDiscovery Staff

The Federal Trade Commission’s Premerger Notification Office logged 185 transactions in April 2026, a 9 percent step-down from March’s 203 but 58 percent above the 117 filings recorded in April 2025 — confirming that the higher filing band of roughly 180 to 230 monthly transactions has held through the first month of FY2026’s second half.

The PNO update means every month of FY2026 so far has come in at 180 transactions or above. The running fiscal-year total now stands at 1,430 transactions across the first seven months of FY2026, which began October 1, 2025. If current run-rates hold despite the volatility that historically affects filings in the back half of the fiscal year — a pattern driven by year-end deal rushes and shifting interest-rate conditions — that pace would reach approximately 2,450 transactions on an annualized basis, outrunning the FY2024 raw total of 2,031 reported transactions (1,973 after adjustments per the FTC’s 47th Annual HSR Report) and modestly above the FY2025 preliminary count of 2,101, both derived from the FTC’s published monthly figures.

The sequential story

March 2026’s 203 transactions, posted last month, marked the high point of the fiscal year so far. April’s 185 steps down from that high but lands within the band traced by the prior six months, all of which fell between 180 and 232 filings. A direct comparison to April 2025 sharpens the picture: that month, 117 transactions were filed as parties continued working through the early weeks of the FTC’s expanded HSR form, which took effect February 10, 2025. The 58 percent year-over-year increase is consistent with both the March 19, 2026, restoration of the pre-February 2025 legacy form following the Fifth Circuit’s decision and a broader rebound in announced deal activity at the high end of the size distribution, though the relative contribution of each is difficult to isolate from monthly counts alone.

HSR Act Merger Transactions Reported – FY 2026 – April 2026

HSR Act Merger Transactions Reported – FY 2025 – 041226

Regulatory environment steadying

Where March captured a regulatory transition in real time — from new form to administrative stay to legacy form within a five-week window — April was the first full month under the restored pre-February 2025 form. The transition traces to Chamber of Commerce v. Federal Trade Commission (No. 6:25-cv-00009, E.D. Tex.), in which Judge Jeremy D. Kernodle granted summary judgment for the plaintiffs on February 12, 2026, holding that the expanded HSR rule exceeded the FTC’s statutory authority and was arbitrary and capricious under the Administrative Procedure Act. The U.S. Court of Appeals for the Fifth Circuit issued an administrative stay on February 19, then denied the FTC’s motion for stay pending appeal on March 19 — leaving the district court’s vacatur in effect and the legacy form immediately operative. The Fifth Circuit’s merits ruling on the underlying appeal remains pending, with such appeals typically resolved within several months to a year. The PNO has continued to accept the new form on a voluntary basis. The Commission and DOJ’s joint public inquiry on the form’s future closes May 26, after which the agencies are expected to outline next steps on a possible new rulemaking. The FTC has stated that it “continues to believe that the prior, nearly 50-year-old form is insufficient to review modern mergers and acquisitions,” and Arnold & Porter notes that, regardless of the outcome of the litigation challenging the updated form, the FTC is considering engaging in a new rulemaking process.

Annual threshold adjustments have been in effect since February 17, 2026. The 2026 size-of-transaction minimum sits at $133.9 million, up from $126.4 million. Transactions valued above $535.5 million are reportable regardless of the size-of-person test. Filing fees on the largest tier reached $2.46 million. According to client alerts from Perkins Coie and Dorsey, the FTC is expected to lift the maximum daily civil penalty for HSR violations to $54,540 once the annual inflation adjustment is finalized in the Federal Register; the current statutory maximum remains $53,088 per day pending publication.

The GDP backdrop

On April 30, the Bureau of Economic Analysis released the advance estimate showing real GDP grew at a 2.0 percent annualized rate in the first quarter — a rebound from 0.5 percent in the fourth quarter of 2025. Real final sales to private domestic purchasers — the BEA’s measure of underlying private demand — accelerated to 2.5 percent from 1.8 percent. The PCE price index jumped to 4.5 percent annualized from 2.9 percent, with core PCE at 4.3 percent. BEA technical notes flagged a partial reversal of fourth-quarter federal compensation losses associated with the 2025 government shutdown, alongside a rebound in business investment led by information processing equipment and software — the AI infrastructure spending that has anchored corporate M&A theses for two years. The BEA’s second estimate is scheduled for release May 28, 2026, and will be the next macro data point shaping deal financing assumptions.

Deal-level composition

The market data behind the filing count tells a bifurcated story. S&P Global Market Intelligence reported global Q1 2026 M&A value at $861.1 billion, the strongest start since 2021 and up 9.7 percent from Q1 2025, while deal count fell 30 percent year over year to 7,924. A single outlier transaction in the S&P Global dataset — Space Exploration Technologies Corp.’s $250 billion acquisition of X.AI LLC — accounted for nearly 30 percent of the firm’s reported global quarterly value, and the headline figure should be read with that concentration in mind. EY-Parthenon’s separate market tracking shows transactions above $100 million up 65 percent in value and 17 percent in volume across February through April 2026, with megadeals above $5 billion up 149 percent in value and 94 percent in volume. FTI Consulting characterized Q1 2026 as disciplined and strategy-led, with strategic buyers driving 82.5 percent of global volume and intra-industry deals at 58.6 percent of activity. BCG’s M&A Sentiment Index stood at 75 in its most recent reading — below the long-term average of 100, though substantially recovered from its late-2022 low point.

HSR Act Merger Transactions Reported – Updated – April 2026

FY2024 reflects the FTC’s adjusted figure (1,973) per the 47th Annual HSR Report. FY2025 and FY2026 are preliminary monthly-sum totals and will be revised downward when the corresponding Annual Reports are issued.

What this means for cybersecurity, information governance, and eDiscovery professionals

For eDiscovery teams, the read is operational. With 1,430 reportable transactions across seven months — and roughly one in four historically valued above $1 billion — the Second Request pipeline supports sustained capacity demand through year-end. Each Second Request typically draws in dozens of custodians, terabytes of structured and unstructured data, and tight statutory timelines. Dechert’s DAMITT Q1 2026 report — a single-firm analytics product rather than an official agency series — tracks four merger investigations of consequence concluded in the quarter, three consent settlements, one abandonment (Alcon/Lensar), and zero contested merger complaints filed by either agency. That mix is consistent with work that leans toward front-end document production and remedy negotiation rather than rear-end litigation discovery. Early termination rates in the same dataset climbed to 35 percent in Q1, below the 50 to 64 percent historical band but a marked improvement over recent years, suggesting some compression in cleared-deal review timelines.

For information governance practitioners, two variables now matter most. The Fifth Circuit’s March 19 restoration of the pre-February 2025 HSR form reduces, for the moment, the volume of ordinary-course documents and narrative submissions parties must marshal at announcement. The FTC/DOJ joint inquiry closing May 26 could reverse that within a rulemaking cycle. Retention schedules, legal-hold triggers, transaction playbooks, and merger-readiness data inventories built around the expanded-form requirements should be revisited but not retired — the agencies have signaled a second-round rulemaking remains on the table. Cross-border deals add a second layer that sits downstream of HSR filing volume rather than driving it: the IEEPA refund process under CBP’s new CAPE functionality, launched April 20, surfaces in contract review, reps-and-warranties analysis, and tariff allocation provisions on any transaction closed during the IEEPA window — work that follows from each filing rather than shaping the filing count itself.

For cybersecurity teams, the active variable is cross-border deal flow — again a downstream effect on diligence depth, not a driver of filing count. Cyber due diligence remains a standard component of acquirer review at this filing volume, with target-side breach history, third-party access controls, identity and data-access governance, and post-close integration risk consistently flagged on transactions above the new $133.9 million threshold. The Section 122 tariff regime introduced on February 24, the planned Section 232 and Section 301 expansions, and active CFIUS-adjacent scrutiny on technology-sector deals raise the bar on supply-chain and foreign-control risk analysis within that diligence. With investment in information processing equipment and software — the AI infrastructure spending underlying many of the megadeals — driving Q1 2026 corporate M&A activity, expect target-side data security posture and AI governance to remain front-and-center diligence items rather than checkbox attestations.

Forward Look

Three near-term data points will frame the rest of FY2026: the BEA second-estimate revision on May 28, the FTC/DOJ public comment record closing on May 26, and the May 2026 PNO release, expected in late June or early July. April’s 185 sets a midpoint rather than a turning point; the question for May and June is whether the band tightens further toward 200 or eases back toward the FY2026 floor of 180 set in January.

With March, April, and Q1 GDP data all in, is the second half of FY2026 better understood as a sustained recovery from the post-new-form trough — or as a higher plateau that may not climb much further before macro pressures bite?

News sources

- FTC Premerger Notification Program (HSR Transactions by Month)

- BEA, Gross Domestic Product (Advance Estimate), 1st Quarter 2026 (April 30, 2026)

- FTC/DOJ FY2024 Hart-Scott-Rodino Annual Report (September 17, 2025)

- FTC/DOJ Joint Public Inquiry on HSR Premerger Notification and Report Form (March 25, 2026)

- FTC Announces 2026 Update of Jurisdictional and Fee Thresholds (January 14, 2026)

- Supreme Court Opinion, Learning Resources, Inc. v. Trump, No. 24-1287 (February 20, 2026)

- Perkins Coie, 2026 Updates to HSR and Interlocking Directorate Thresholds (January 16, 2026)

- Dorsey, Increase in HSR Reportability Thresholds and Filing Fees and Other HSR Developments (January 26, 2026)

- Dechert, DAMITT Q1 2026: Restrained Merger Enforcement Continues With Shorter Timelines

- Arnold & Porter, Antitrust Agency Insights: First Quarter 2026 (April 15, 2026)

- Holland & Knight, Supreme Court Strikes Down IEEPA Tariffs: What Importers Need to Know Now

- White & Case, United States Terminates IEEPA-Based Tariffs Following Supreme Court Decision

- Ropes & Gray, Supreme Court Strikes Down IEEPA Tariffs — Key Takeaways

- S&P Global, Global M&A by the Numbers: Q1 2026

- EY, M&A Activity Insights: April 2026

- FTI Consulting, Global M&A Q1 2026 Market Update

- BCG, M&A Outlook 2026: Expectations Are High — Again

- A&O Shearman, HSR in Transition: FY2024 HSR Annual Report Shows Legacy Trends

- LENSAR, Inc. Form 8-K, Merger Termination (March 16, 2026)

- HSR Filings Hit 203 in March 2026 as Court Overturns Expanded Form and GDP Slips to 0.5%

Assisted by GAI and LLM Technologies

Additional Reading

- HSR Act Reporting: A ComplexDiscovery Chronology

- FTC Annual Competition Reports (Hart-Scott-Rodino Act Reports)

Source: ComplexDiscovery OÜ

ComplexDiscovery’s mission is to enable clarity for complex decisions by providing independent, data‑driven reporting, research, and commentary that make digital risk, legal technology, and regulatory change more legible for practitioners, policymakers, and business leaders.

The post Second request pipeline watch: April HSR filings, Q1 GDP, and form rulemaking window closing appeared first on ComplexDiscovery.