By Louis Lehot. From garage to global, since Y2K. A read on Rob Bartlett’s June 2026 Jefferies Software Valuation Update, for the founders, CEOs, and directors who have to make a decision about it.

Friends,

I am not a banker, and I do not call markets. But I read Rob Bartlett’s monthly Jefferies note the way I read an indemnity, which is to say closely, because it tells me what the other side already knows. The June 2026 update landed last week. It quietly rewrites the comp your company gets measured against the next time you raise or sell, and you should know about it before your next board meeting, not after.

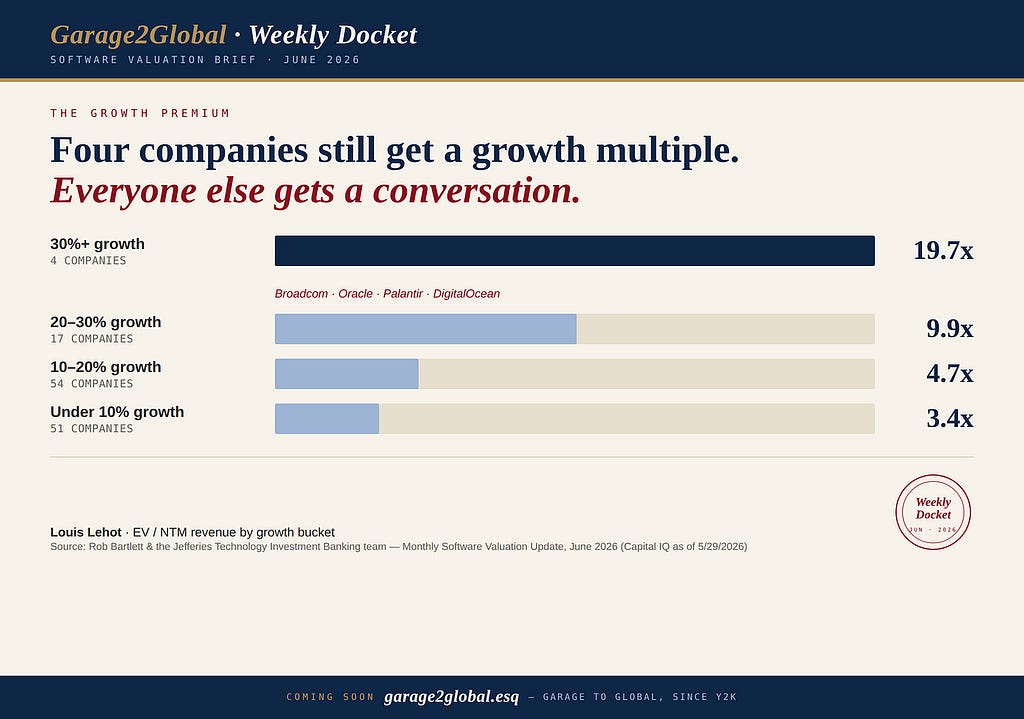

Here is the number that should reset the conversation. As of late May, exactly four public software companies are growing revenue north of 30 percent next year. Broadcom. Oracle. Palantir. DigitalOcean. Four. They trade near 19.7 times forward revenue. Everybody else lives well below that. The 10 to 20 percent growth crowd trades around 4.7 times. Roughly 85 percent of public software now grows under 20 percent, against about half the universe at the 2021 peak. The high-growth club did not get re-rated. It got depopulated.

What is actually driving this

This is not a rate story. It is the SaaSpocalypse. That is the name the trading desks gave the February selloff that wiped out something like 285 billion dollars of software value in roughly forty-eight hours. No earnings miss. No rate hike. No recession to blame it on. The trigger was a batch of Claude Cowork plugins for legal, financial, and sales workflows, and the market asked the one question that now hangs over every per-seat business. Why pay for ten licenses when one agent does the work?

I have watched a lot of technology shifts in this valley over thirty years. This one is different. Coding agents like Claude Code and OpenAI’s Codex have collapsed the cost of building software. Think about how a project used to be shaped. Three weeks on design and architecture. Eight weeks of coding and engineering. Three weeks getting it deployed. The engineering in the middle was the expensive part, the part you staffed up for, and it is exactly what SaaS sold against. Do not hire eight engineers for eight weeks. Just buy the seat.

That shape has flipped into a barbell. Design still takes a couple of weeks, because deciding what to build is still human judgment. Deployment, integration, and security review still take one to three weeks, because getting software safely into a real enterprise is no faster than it ever was. But the coding in the middle has gone from eight weeks to somewhere between a day and a week. The bottlenecks moved to the two ends. The middle, the part SaaS got paid for, has nearly disappeared.

That is the whole ballgame for valuation. When the expensive parts are judgment at the front and trust at the back, and a generic SaaS license solves neither one, the old build-versus-buy math tips toward build. A customer who does not like a renewal quote can credibly threaten to stand up its own internal tool in days. Even when it does not, the threat alone drags down what a vendor can charge. Klarna walking away from its CRM in 2024 was not a stunt. It was the leading edge.

I have made this point in this newsletter for months, and the market keeps proving it out. Claude Code is not eating startups. It is eating SaaS. The traditional software business, the one that sold seats and renewed them every year on switching costs, is the one under pressure, and it has poisoned the well for investment. No serious buyer or sponsor wants to underwrite recurring revenue that a competitor, or the customer itself, could rebuild in a weekend with a tool that did not exist eighteen months ago. When you cannot tell whether a target’s ARR is durable or a melting ice cube, you do not pay a premium for it. You do not pay at all. That uncertainty, more than any move in rates, is what has frozen the software M&A market.

The mechanics follow. Seat-based pricing was beautiful because revenue grew automatically as headcount grew. Agents break that link, and may run it backward, since an AI-augmented worker needs fewer seats, not more. Net revenue retention, the metric that justified premium multiples for a decade, softens the moment expansion stops happening on its own. Median public SaaS growth has already slowed into the low teens, and some smart people argue a big chunk of that is just enterprise budget rerouting to Anthropic and OpenAI. For the first time I can remember, software as a group trades at a discount to the S&P 500.

Here is the honest part, and the part I tell every board. Nobody actually knows yet whether AI eats SaaS or feeds it. The bear case is structural. Seats compress, features commoditize, the agent becomes the interface and the app underneath becomes plumbing. The bull case is that this is a snake shedding its skin. The shiny AI-native point tools get adopted fast and churn out just as fast, because narrow tasks where every model produces similar output have no switching cost, while the incumbents with real data, regulated-industry trust, and deep workflow integration are the ones that survive and re-rate. Both cases are credible. That unresolved tension, not some number on a screen, is what the multiples are pricing. Jake Saper at Emergence Capital called the contrast between Cursor and Claude Code the canary in the coal mine. One product owns the developer’s workflow. The other just executes the task. Developers keep choosing the one that does the work. Workflow stickiness, the most-cited moat in every Series C deck since 2018, now has to be re-earned from scratch.

Why this changes the framework, not just the scoreboard

Against all of that, Bartlett offers GRAF, a Growth-Adjusted Rule of 40. The premise is one I flag for any founder still putting a tidy Rule-of-40 score on a slide. Growth and margin are not interchangeable. His two-factor regression puts revenue growth at roughly 2.4 times the valuation weight of free-cash-flow margin. A company that hit 40 by grinding to a fat margin on thin growth is not the same asset as one that hit 40 on real growth. In a market this nervous about whether growth even lasts, buyers have stopped pretending those two are the same. On that weighted basis, software trades around 0.23 times today, down from 0.52 times in November 2021.

Where the comps meet the deal terms

This is where the valuation story runs into the deal-points studies I keep on the shelf. The SRS Acquiom M&A Deal Terms Study has shown earnouts climbing as the tool of choice for bridging a valuation gap, and there is no wider gap than the one between a seller who believes its growth is durable and a buyer quietly modeling seat erosion out to 2030. The earnout is the bridge. Its structure, which milestones gate the payout and who controls the roadmap after close, now matters more than the headline number. The ABA Private Target Deal Points Study tracks the normalization of rep-and-warranty insurance and the erosion of seller-friendly MAE definitions. In a market this jumpy, buyers have the leverage, and you see it in longer survival periods, tighter baskets, and diligence that goes straight at net revenue retention and AI exposure. Show us the moat, or take a lower number. That is the sentence of 2026.

What I tell a board this quarter

Three things. Benchmark against the 10 to 20 percent bucket near 4.7 times, not your 2021 print, and be ready to say in plain English why AI is a tailwind to your retention and not a solvent on your seats. Treat growth and margin as separately priced. GRAF is a useful discipline even if you never say the acronym out loud. And expect the gap between your number and a buyer’s to get papered over with structure, so bring your counsel into the terms conversation early, not after you have shaken hands on price.

The market did not close. It got precise about what it will pay for, and what it is pricing right now is a genuine open question about the next decade of software. That is a reckoning for anybody who assumed the multiple always comes back. It is an opening for the operators who can prove the moat is real.

Talk soon.

— Louis